Mortgage Rate Recap and Predictions For Week Ending October 19th, 2018

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

Yesterday the Fed released the Beige Book which contained an even stronger emphasis on the impact of tariffs and labor shortages than the previous two publications. Along with that, all twelve districts in the U.S. said the economy is expanding moderately or at a moderate pace in their region.

The issue of labor shortages isn’t new news, but employers are stepping up their enticements to try and lure potential job candidates, which include job training and no drug testing. They aren’t, however, increasing wage levels but offer non-cash benefits to entice workers.

Pending home sales in September came in at 0.5%, up from -1.9% in August, and that at a time of rising interest rates to levels higher than in 2011. Along with that positive sign, realtors are reporting increases in property listings on the National Association of Realtors (NAR) Multiple Listing Service (MLS). This is the first increase in listings nationally in a long time.

On Friday, October 26th, GDP will be released, and the market is bracing for the number. Analysists believe the numbers would need to be below 3% for interest rates to fall. Market expectations put the figure between 3.3% and 3.9%, which would cause interest rates to increase.

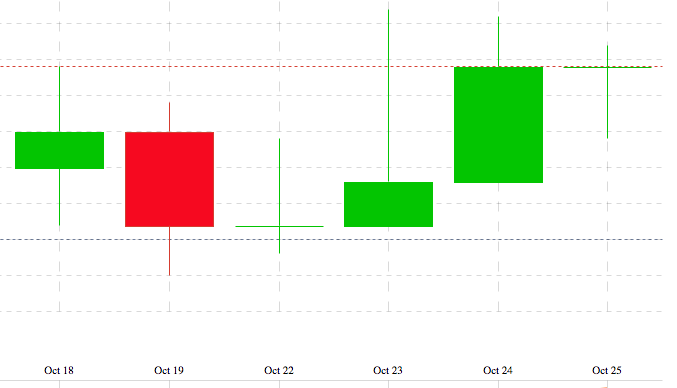

Mortgage Rates Increase

This candlestick chart below covers the past weeks’ Mortgage Backed Securities (MBS) activity and the impact on interest rates. MBS were at 102.35 at the close on Oct 18th and closed trading at 102.44 October 25th. MBS directly impact mortgage rates, and the days with red indicate higher rates and those with green – lower rates.

This week’s Mortgage Banking Associations‘ (MBA) weekly rate survey shows effective rates increased for all loan products, with the exception of the 15-year fixed which remained unchanged. The information below applies to all loans with an 80% loan-to-value.

Per the MBA weekly survey: “The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) increased to its highest level since February 2011, 5.11 percent from 5.10 percent, with points decreasing to 0.52 from 0.55 (including the origination fee.)”

1 point in cost = 1% of the loan amount

“The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $453,100) increased to 5.01 percent from 4.98 percent, with points decreasing to 0.28 from 0.34 (including the origination fee.)”

“The average contract interest rate for 15-year fixed-rate mortgages remained unchanged at 4.50 percent, with points increasing to 0.55 from 0.54 (including the origination fee.)”

“The average contract interest rate for 5/1 ARMs its highest level since the series began in 2011, 4.47 percent from 4.34 percent, with points increasing to 0.37 from 0.35 (including the origination fee.)”

Mortgage Rate Activity and Predictions

Bankrate’s weekly survey of mortgage and economic experts, countrywide, shows the majority (23%) predicting interest rates will remain unchanged next week (plus or minus two basis points), with the remaining split between 31% predicting rates will increase and the majority of 46% expecting interest rates to decrease next week.

My prediction is that rates will drop this week, as quoted in the Bankrate report, “Mortgage rates will drop. After a steep jump at the beginning of the month, mortgage rates have settled down in the last two weeks. Stock markets have been volatile, corporate earnings not quite what the market expected, and the yield on the U.S. 10-year Treasury has fallen a tad. All of these factors should help the demand for mortgage-backed securities, which consequently, should result in lower mortgage rates for the borrowers.”

The chart below, from Freddie Mac’s weekly mortgage survey, shows conforming rates had a very slight increase for the week of October 18th to October 25th, for 30Y fixed and 15Y fixed.

Freddie Mac’s weekly mortgage survey noted, “Despite volatility in the stock market, the 30-year fixed-rate mortgage inched forward just 1 basis point to 4.86 percent this week. We expect rates to continue to rise, which will put downward pressure on homebuying activity. While higher borrowing costs will keep some people out of the market, buyers with more flexibility could take advantage of the decreased competition.“

Mortgage Rate Lock Advice

No question locking in an interest rate now, ahead of tomorrow’s GDP release, is the best advice. At the same time, the majority of mortgage professionals surveyed believe rates will fall next week. If rates decrease, you can expect the difference to be small enough to make floating risky.

Related Posts

- 98The last three weeks delivered increasing mortgage rates and the coming week is shaping up to be a repeat. What's behind this negative break from the summer doldrums rates have languished in is a steady sign that inflation is substantially above the Feds target of 2%. The latest CPI 4-week…

- 98Despite continued tariff threats and retaliations between the US and China, the markets are reacting more to the continuing strength in the economy, led by a strong job market. Overall, the impact on mortgage rates has been a very slight increase that looks more like a sideways movement. Globally, aside…

- 98Mortgage rates have virtually treaded water for the summer, and it looks like that pattern will continue at least for another week. At this point, nearing the end of the week of July 23rd, the economic data released was Durable Goods and the Weekly Jobless claims, and both came in…

- 97Most of the economic data released this week has been in line with predictions and expectations resulting in a little to no impact on the long-term bond market, which has a direct effect on mortgage rates. Mortgage Backed Securities (MBS) reacted negatively yesterday to two factors: oil moving above $71/barrel,…

- 97This week's news has had little impact on mortgage rates. Trade war concerns shifted from steel and aluminum tariffs to China's history of piracy issues in technology and intellectual property. The majority of the media commentary is around the appointment of Larry Kudlow as White House economic advisor. Kudlow has…