My Offer for a Home Purchase Is Accepted! Now What?

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

You finally get the call from your Realtor and hear the words “They accepted your offer!” It’s been a long, hard road to find a home you love, and harder still for a seller to agree to let YOU be their buyer. Now you’ve crossed this hurdle, but you’re not sure what happens next. Does your Realtor take it from here or your loan officer? Are you supposed to do anything?

The answer is – it’s a team effort — the team of professionals you assembled before making offers, and that includes you. So get ready, because the first couple of weeks move very quickly, with paper flying everywhere! Then things will slow down as the pieces of the loan process start falling into place.

During your Realtor’s first call about the accepted offer, they also let you know it was time to send an earnest money deposit to escrow as part of the purchase contract. The Escrow Officer works with you to collect your deposit, holding it in an escrow account until the transaction closes. Your lender will also exchange information with escrow, regarding your purchase, at the beginning of the loan process.

You’ll continue to work with your Realtor going through inspections and other steps related to the property, but your loan process needs the majority of your attention at the beginning. In this post, I’m going to outline all the steps in the mortgage process and give you a roadmap so you’ll know what to expect. Keep one thing in mind: “time is of the essence,” when it comes to the mortgage process, and that’s especially important in the first two weeks.

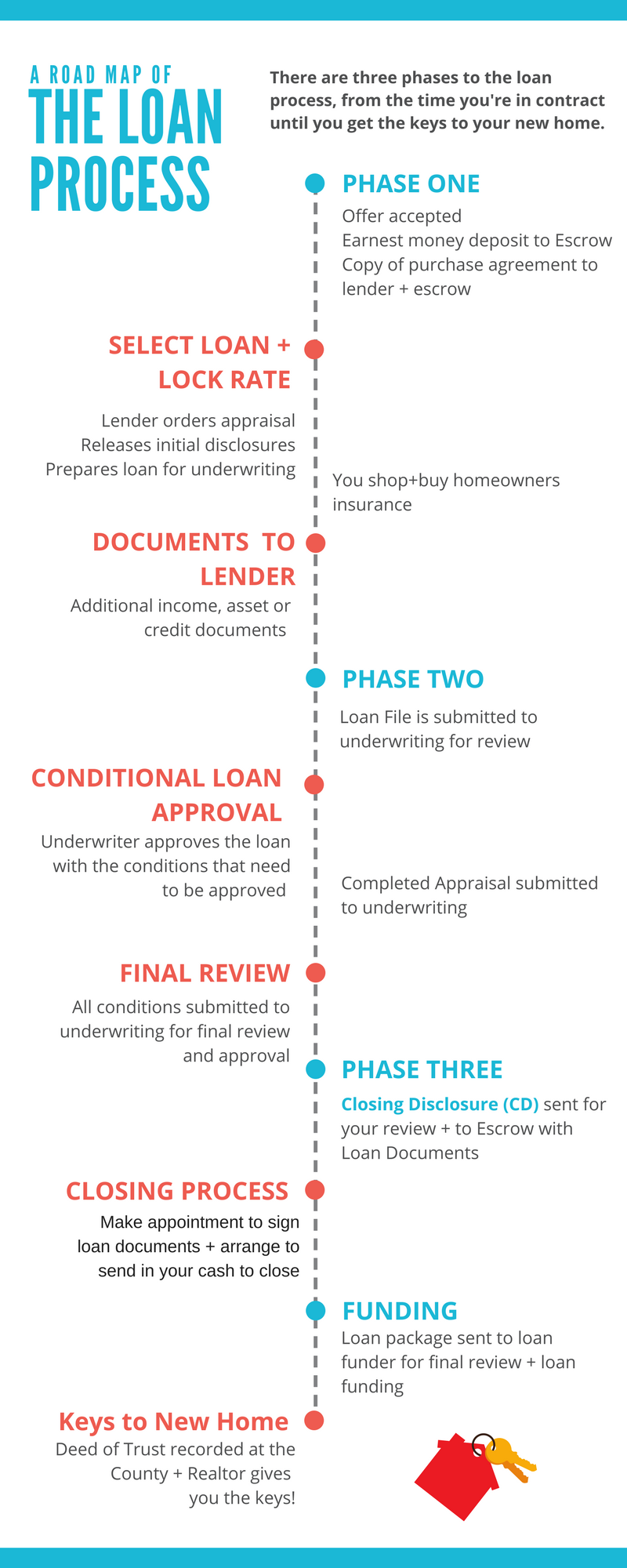

There are three main phases of the loan process. Phase one focuses on gathering documents, delivering your initial loan disclosures and preparing the file for underwriting. The primary goal of this phase is to assemble as complete a loan package as possible before the underwriter performs their review.

It begins, however, with choosing your loan program and locking in the interest rate. These two steps will remove a lot of anxiety and help avoid any surprises during the loan or at closing. Once the rate is locked in, we’ll also:

- Order the appraisal

- Prepare and issue your initial loan disclosures

- Gather any remaining documents (regarding income, assets or credit)

You may also need to write Letters of Explanations for the benefit of the underwriter. These can include details of a recent raise, a new credit card or unusually large deposits. It’s also time for you to begin to shop for and choose your homeowner’s insurance coverage.

Underwriting is the main event in phase two of the loan process. If you, the loan officer and the processor have done all you can to submit a well-documented loan file, the initial underwriting review should be smooth, resulting in a Conditional Loan Approval. This means that the loan is approved as long as certain conditions satisfy the underwriter. Examples of these conditions can be requests for a written verification of employment to document bonus income, or clarification and missing signatures from the purchase contract.

Again, time is of the essence to gather these conditions and submit them to underwriting for the final review. The completed appraisal is reviewed with the loan conditions, as well. As you can see, underwriting occurs in two parts, and it’s complete when you receive final loan approval.

In phase three, your close of escrow (closing of the transaction) is right around the corner. First, the Closing Disclosure (CD) is prepared and released so you can review all the actual costs of the transaction. You are required to wait 3 business days after the CD is issued before the final loan documents can be signed. The loan documents are sent to escrow by the lender. The Escrow Officer will use the loan documents to determine how much cash is needed (cash-to-close) to close the transaction, in addition to the loan amount.

You need to schedule an appointment to sign the loan and purchase documents and have your funds arrive in escrow at or before the signing. If your schedule is crazy and going to the escrow office for signing seems impossible, you can request for a mobile notary to bring the documents for your signature where and when it’s convenient.

After the documents are signed, the escrow officer will ship them to a member of the loan team known as the funder. The funder reviews the package for accuracy and may reach out to everyone for minor corrections or changes that could include more signatures on your part. It’s not uncommon, so be flexible and provide whatever is needed. You’ll notice everyone on your team engaging and cooperating to finalize your transaction.

To close the transaction the lender wires the loan funds to escrow, and the escrow officer records the new deed of trust with the county. The recorded deed is the official final step, and your Realtor will then be free to present you with the keys! This step differs in order and timing depending on which state your purchase occurs. Some states also use Closing Attorneys to handle all of the duties described here instead of an Escrow Officer.

Knowing what happens after your offer is accepted will help remove a little fear of the unknown from the process of buying a home and getting a mortgage. Working as a team with your Realtor, lender and escrow officer/closing attorney makes all the difference in your experience. The quick responses and regular communication by all team members will get you the keys to your home before you know it!

Related Posts

- 84Home insurance is a $70 billion industry. According to a recent report, 95 percent of homes in the U.S. are insured. There are a number of benefits associated with home insurance. For homeowners, having a home insurance policy means being able to recover from financial blows that often arise as…

- 82The process of buying a home is just that - a process. Like with any major process there are a multitude of potential missteps to avoid. Let's discuss three huge ones. Failing to Consider Your Spending Habits and Expenses Lenders qualify you for what you technically can afford based on…

- 79Millennials have two things in common, other than their age, they have student loan debt and they make up the primary market of first-time homebuyers. Sometimes, they have a lot of student loan debt which affects their ability - or perceived ability - to remove their renter tag and add…

- 79Whether you're a seasoned or new investor, calculating cash flow on a potential rental property is a critical part of your analysis before buying. You need to make sure you crunch the numbers completely before deciding to invest your money and getting the cash flow calculation right might be the…

- 74Even with a minor slow down in home sales during recent months, desirable properties are still getting multiple offers. Make no mistake, we are still very much in a seller's market. Available housing inventory ranges from low to non-existent in many neighborhoods. With low mortgage rates still pervasive and rapidly…