How to Calculate Cash Flow When Buying an Investment Property

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

Whether you’re a seasoned or new investor, calculating cash flow on a potential rental property is a critical part of your analysis before buying. You need to make sure you crunch the numbers completely before deciding to invest your money and getting the cash flow calculation right might be the best investment you can make.

Basic Ingredients of Cash Flow

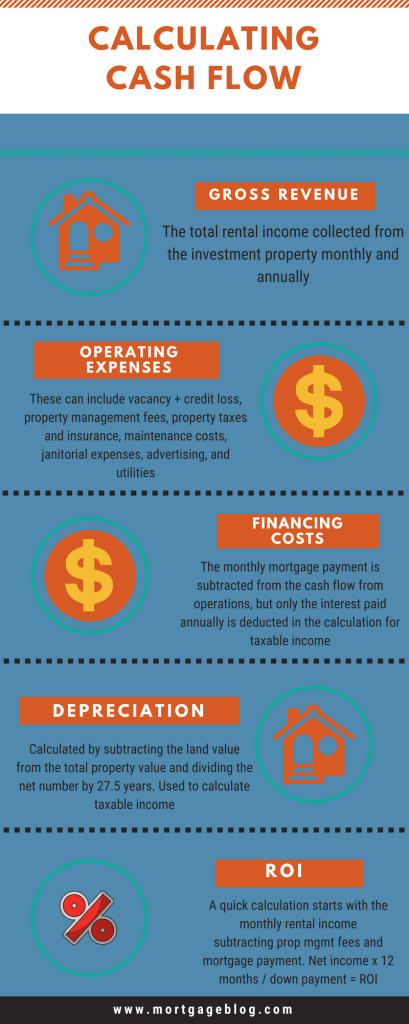

First, gather the property’s current and potential rental income. Whether you’re buying one unit (single family home) or a multi-unit property, find out what the current rental income is and compare it to current rents in the area. Once you have this information you will be able to set one number in the cash flow calculation: Gross Revenue.

Next, detail the operating expenses you can reasonably expect from owning the property. These include a reserve for vacancy and credit loss, fees for property management, property taxes and insurance, maintenance and repairs, and utilities. Depending on the type of property you purchase the operating expenses can also include legal and accounting fees, janitorial costs, advertising, and supplies.

Credit loss refers to the months when a tenant fails to pay their rent while occupying your unit. Vacancy, on the other hand, is an estimate of those months when the unit is not rented (and not earning any income for you).

Check today’s interest rate for buying an Investment Property

Gross Revenue – Operating Expenses = Net Operating Income (NOI)

This calculation will give you the estimated net operating income, but you still need to account for the financing costs, taxes and potential capital expenditures. Depending on the age and condition of the property, there may be deferred maintenance that will require an infusion of additional capital after you purchase the property. These can include replacing the roof, repair or replace heating + air systems, repaving the driveway, replacing appliances, and miscellaneous structural repairs. Subtract a reasonable percentage of the projected NOI as a reserve for these capital expenditures.

NOI – Capital Expense Reserves = Cash Flow from Operations (CFO)

At this point in your calculation, you can deduct the cost of the mortgage payment (principal and interest) from the CFO. For example, a rental property with a purchase price of $200,000 with a $40,000 down payment (20% of the purchase price), will require a $160,000 mortgage. A 30 year fixed rate mortgage at 4.63% will have a monthly principal + interest payment of $1330.00. Subtract that from the CFO to determine the actual cash flow.

Don’t Forget the Taxes

Calculating the taxes due on your rental property is a slightly different equation, but paying those taxes does impact your actual cash flow. The equation looks like this:

Gross Revenue – Operating Expenses = NOI

NOI – (Interest Expense + depreciation) = taxable income

You will only deduct the interest portion of your mortgage payment for taxable income, as the rest of the payment reduces your principal, increasing the equity you have in the property. The other deduction, depreciation, is a non-cash expense. To calculate depreciation you need the value of the property excluding the value of the land. Only the building is depreciated over 27.5 years.

Property Value – Land Value/ 27.5 years = annual depreciation

In the example above, the $200,000 property has a $45,000 land value, leaving $155,000 to be depreciated over 27.5 years, or $5636/year. The interest paid on the $160,000 mortgage for the first year is $7355. The total amount subtracted from the NOI is $5636 + $7355 = $12,991, and the net amount is the taxable income for the property.

Get Pre-approved to buy an Investment PropertyGet Pre-approved to buy an Investment Property

Cash Flow and ROI

Using cash flow to calculate the return on investment (ROI) can be quick and simple. Starting with the gross monthly income, subtract the monthly mortgage payment and property management fees, and then annualize the number. Divide that amount into the cash down payment, and you’ll have a rough estimate of the ROI. Using the earlier example of the $200,000 rental property purchase with $40,000 down payment, assume monthly rent of $1600 and property mgmt fees of $80.

Gross income $1600.00

Princ+Int -$1330.33

Prop Mgmt -$ 80.00

Monthly Inc $ 189.67

Annual Inc $2276.04 / $40,000 (down payment) = 5.69% ROI

Once you have detailed out the operating expenses of a target property, you’ll be able to assess the true potential cash flow a property might offer. Don’t forget to account for the accumulation of equity through debt repayment as well as the appreciation of the property when evaluating the potential for the investment.

Want to get the “Calculating Cash Flow Spreadsheet”? Email me at [email protected]

You May Also Like to Read:

Best Real Estate Markets To Invest in 2018

Related Posts

- 82Millennials have two things in common, other than their age, they have student loan debt and they make up the primary market of first-time homebuyers. Sometimes, they have a lot of student loan debt which affects their ability - or perceived ability - to remove their renter tag and add…

- 81The process of buying a home is just that - a process. Like with any major process there are a multitude of potential missteps to avoid. Let's discuss three huge ones. Failing to Consider Your Spending Habits and Expenses Lenders qualify you for what you technically can afford based on…

- 79You finally get the call from your Realtor and hear the words “They accepted your offer!” It’s been a long, hard road to find a home you love, and harder still for a seller to agree to let YOU be their buyer. Now you’ve crossed this hurdle, but you’re not…

- 65Home insurance is a $70 billion industry. According to a recent report, 95 percent of homes in the U.S. are insured. There are a number of benefits associated with home insurance. For homeowners, having a home insurance policy means being able to recover from financial blows that often arise as…

- 63With the Remodeling market size expected to touch a massive $269 billion by 2025, it was time for Freddie Mac to jump into the Renovation loan marketplace. Especially given that the Federal Housing Administration and Fannie Mae have this kind of loan in place for, what, years now. Freddie Mac’s…