Mortgage Rate Recap and Outlook For Week Ending June 8, 2018

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

Without any geopolitical flare-ups over the last week, the impact of economic data has been very mild with no measurable effect on the markets or mortgage rates. The biggest job news was the filing of Jobless claims coming in slightly below predictions, but the 4-week moving average ticked up to 225,500 – amazingly low.

Global economic news has also had little effect on mortgage rates, with continued talk of a timeline to end qualitative easing (QE) in the ECB the only topic of import.

While the markets are quiet now, all eyes are on the meeting of the leaders of the seven industrialized nations (G7) beginning tomorrow in Toronto. In the last few days leading up to the meeting, there have been several ‘shots across the bow’ of potential pushback on several trade agreements and even retaliation against recent US protectionist economic policies.

Even Putin is trying to ‘join the club’ with EU countries in calling out the US for perceived bullying tactics. The reality of what transpires in the G7 meetings and the impact it may have on the long-term bond market remains to be seen.

Mortgage Rates Improved

This candlestick chart below covers this weeks’ Mortgage Backed Securities (MBS) activity and the impact on interest rates. Rates improved slightly over this past week, although the candlestick chart shows more red than green. MBS directly impact mortgage rates, and the days with red indicate higher and green lower rates.

This week’s Mortgage Banking Associations’ (MBA) weekly rate survey shows effective rates decreased for all loan products with an 80% loan-to-value.

Per the MBA weekly survey: “The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($453,100 or less) decreased to 4.75 percent from 4.84 percent, with points decreasing to 0.46 from 0.47 (including the origination fee.)”

1 point in cost = 1% of the loan amount

“The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $453,100) decreased to 4.70 percent from 4.73 percent, with points decreasing to 0.35 from 0.36 (including the origination fee.)”

“The average contract interest rate for 15-year fixed-rate mortgages decreased to 4.21 percent from 4.24 percent, with points decreasing to 0.50 from 0.51 (including the origination fee.)”

“The average contract interest rate for 5/1 ARMs decreased to 4.08 percent from 4.11 percent, with points decreasing to 0.41 from 0.62 (including the origination fee.)”

Mortgage Rates Next Week

Bankrate’s weekly survey of mortgage and economic experts, countrywide, shows a majority (62%) predicting interest rates will increase this coming week (plus or minus two basis points), and 23% predicting a fall in rates next week. The remaining 15% predict rates will remain unchanged.

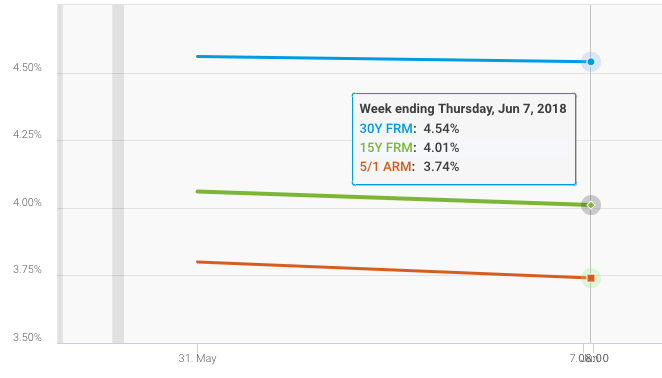

The chart below, from Freddie Mac’s weekly mortgage survey, shows conforming rates decreasing slightly over the last week, June 1st to June 7th, for 30Y fixed, 15Y fixed and the 5/1 ARM.

In Freddie Mac’s weekly mortgage survey it was noted that “Mortgage rates dipped for the second consecutive week.

Homebuyers have taken advantage of the recent moderation in rates, which led to a 4 percent increase in purchase applications last week.

Although demand has remained steadfast against the backdrop of this year’s higher borrowing costs, it’s important to note that the growth rate of purchase loan balances has moderated so far this year – and particularly since March. This slowdown indicates that buyers are having difficulty stretching to keep up with the pace of home-price growth.

While the very healthy job market continues to fuel interest in buying a home, the supply shortages in most markets are pushing prices higher and currently keeping sales at a standstill. Listings for new and existing homes need to increase in the months ahead to moderate price growth and reignite sales activity.”

Lock Advice

Recommend locking in a rate now if you are purchasing or refinancing. There is not enough potential market improvement to support taking any risk in floating right now.

Related Posts

- 96Jobs data released this week was very positive, with jobless claims at their lowest levels since 1969. On top of that, the frequently volatile Philadelphia Fed Business Outlook Survey came in at 34.4 versus the predicted 21.0. As far as geopolitical events having an impact on trading we had some…

- 95As of the end of April, the year-over-year (YOY) nationwide increase in home prices is at 6.4%, based on actual appraisals for all loans sold to Fannie Mae, Freddie Mac or Ginnie Mae (all conforming and government loans.) While it's now almost the end of June, and the data is…

- 95The market continued to improve in the early part of the week, led by the drama coming from Italy and a sharp drop in oil prices. These issues are no longer impacting the markets, and mid-week Mortgage Backed Securities began to move back into the red, creating a slight pressure…

- 95Piggybacking on low mortgage rates, the refinance applications are on a rise. Refinance volume has pushed total mortgage volume up and it is nearly 150% above where it was, this week last year. The data, however, is not as reliable given that Thanksgiving fell a week earlier last year. To…

- 93When the bond yield curve had inverted in late August, the USA began to harbor recessionary fears. These fears have since diluted; a trend reflected by a slight increase in the mortgage rates over the last couple of months. America's manufacturing sector is still under the pump and this creates…