Is Affordability Becoming a Problem for US Real Estate?

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

What do you do when the free market prices the average – sometimes even the exceptional – American family out of owning a home? The answer used to be simple, people would just rent.

In many markets – most major metro area – rents are increasing at rates equal to, or higher than, home values? Something has to give.

You have to have somewhere to live whether you own it, rent or – in some cases – drive it.

So how do we approach the affordability issue that many markets are experiencing? Where can you get the most bang for your buck – owning or renting?

Get Pre-Approved to buy a Home

We first need to understand this is not a problem solely for the coasts.

In fact, based on the Housing Affordability Index, the Midwest is the hardest hit. They may have the lowest median home price at $201,500, but they also – by a mile – have the lowest median income at $36,720.

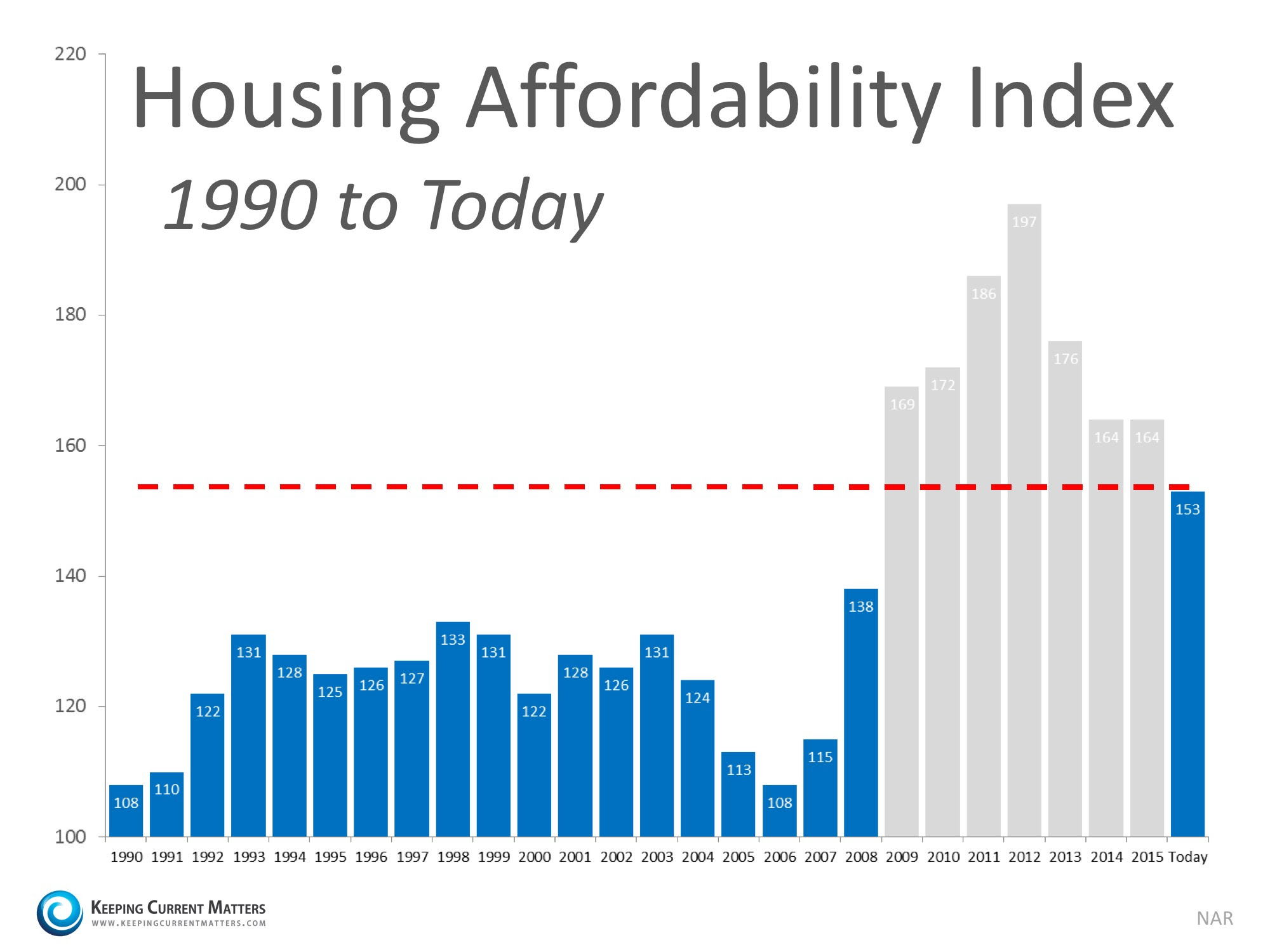

The Housing Affordability Index (HAI) for a given area is calculated by the share of homes sold in that area that would have been affordable to a family earning the local median income, based on standard mortgage underwriting criteria.

It’s a pretty simple calculation with two components – income and housing cost.

A value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.

An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment and a qualifying ratio of 25 percent.

For example, a composite HAI of 120.0 means a family earning the median family income has 120% of the income necessary to qualify for a conventional loan covering 80 percent of a median-priced existing single-family home.

The Midwest has a HAI of 186.8 – that’s potential trouble.

In San Francisco, where the median income is $83,000, about 61 percent of one-bedroom homes are renting for $3,000 or more per month – that’s problematic too.

The median income in Oakland is $47,000, which translates to $1,175/month for rent, but the average monthly rent in Oakland is $3,000.

An entry-level teacher in the Oakland Unified School District makes just above the median.

Entry-level pay for police in Oakland is $70,000, meaning no more than $1,750 a month should be allocated towards housing.

You can see the income needed to buy in California and other West Coast markets is significant as well.

As a nation, the Housing Affordability Index sits at 153.3 according to the National Association of Realtors

That’s actually down some from the recent high water mark of 173.8 posted in February of 2016, but don’t let the Affordability Index dip fool you though.

That’s simply a side effect of lower mortgage rates driven down by global unrest (especially Brexit) and ripe economic conditions at home.

Home prices – rent too – are still rising nearly everywhere. When rates go up so do the chances of further housing affordability chagrin. What then?

Remember that the index is based on a 20 percent down payment too. Rising home prices mean rising down payments.

The average home price nationwide is $249,800. You’ll need approximately $50,000 just for the down payment.

That doesn’t include closing costs, escrows and other costs associated with buying a home – new furniture, moving expenses, home inspections or simply a coat of fresh paint.

In San Jose, California the median price just crossed a cool million, first metro to ever reach that mark.

Hey brother, can you spare some change?

How much ya need?

Oh, around $200,000 should do it.

You’ll notice below, however, that San Jose and Silicon Valley do not crack the list of cities with the least affordable housing.

As long as the tech industry – and the cabbage being earned in it – keeps its pace they likely won’t appear on the list either.

Wondering where your city sits on the list? Here are the cities with the most and least affordable housing:

Get live rate quote customized for you

Top 10 most affordable cities

| Metro area | Median home price | Salary needed |

|---|---|---|

| Pittsburgh | $140,500 | $32,390.09 |

| Cleveland | $138,100 | $34,433.95 |

| Cincinnati | $160,600 | $37,179.18 |

| St. Louis | $170,300 | $38,131.22 |

| Detroit | $164,200 | $38,541.83 |

| Atlanta | $192,000 | $40,092.12 |

| Phoenix | $234,700 | $44,715.99 |

| Tampa | $199,900 | $44,874.70 |

| San Antonio | $210,500 | $48,752.98 |

| Orlando | $223,000 | $49,382.26 |

Top 10 least affordable cities

| Metro area | Median home price | Salary needed |

|---|---|---|

| San Francisco | $885,600 | $161,947.60 |

| San Diego | $589,900 | $109,440.97 |

| Los Angeles | $480,000 | $92,091.89 |

| Boston | $435,800 | $87,556.61 |

| New York City | $395,400 | $86,215.44 |

| Seattle | $420,500 | $82,670.73 |

| Washington, D.C. | $406,900 | $81,940.22 |

| Denver | $394,400 | $72,847.39 |

| Portland, Oregon | $356,700 | $70,613.37 |

| Sacramento | $323,700 | $65,362.63 |

California dominates the least affordable list clearly, but there’s a lot of things California wins – best weather, awesome natural landscape, high paying jobs, progressive mindset – so no surprise there.

What Are My Mortgage Options in More Expensive Markets?

Well, for starters you don’t have to put 20 percent down.

In addition to lower down-payment mortgage loan options – like FHA, USDA and Fannie Mae’s HomeReady – there are also subsidies and government programs available that help the housing ends meet for those with incomes below the HUD median average for that county.

In some cases, there are state and local grants for would be homebuyers – especially those at 80 percent of the median county income or less.

Some of those grants are “soft” second mortgages which simply means that you’ll not have a payment and only have to repay should you sell your home prior to a specified amount of time – typically 5 years.

They assist with the down payment and effectively reduce the cost of the home since they generally require no monthly payment if the terms of the program are met.

HUD offers programs too. The Good Neighbor Next Door program offers homes for sale that were foreclosed with an FHA loan in place to our honorable community servants – Teachers, Firefighters & Police Officers – at a 50 percent discount.

Check out how you can buy a $1.8M California home with only 10% down payment

How Do We Fix This Affordability Problem?!

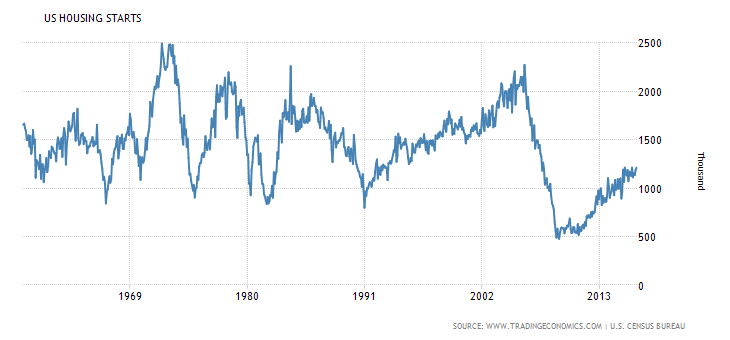

Build. Build some more. Build again.

This is an inventory issue, pure and simple. When the 2007 crash happened everyone stopped building. Builders either went under or got spooked by the market and shut construction down for 5+ years. Take a look yourself…

Meanwhile, babies are being delivered and millennials are forming households – the nation is growing. People need more space, they need more housing and that chart scares me.

When construction started to approach normal in 2014 builders focused on the higher – more profitable – end of the market. They still are.

But, that’ll change soon because that market is over-served and has left a swath of the home buying populace out in the cold – first time homebuyers.

Starter homes barely exist in 2016. When one pops on the market it goes under-contract the next day.

Smart home builders are already making the switch to meet the demand. Unfortunately – or fortunately if you’re a builder who recognized the pent-up demand and moved toward it – not nearly enough builders have placed emphasis on this demographic.

Regardless, if you’re unhappy with simply handing a landlord your rent money every month with no tax deductions, no control, no equity creation and no permanent ties to your neighborhood, than you owe yourself – at least – a quick call to your loan officer for a consultation that lays out all your housing options.

You may find that renting is best, but you’ll likely find otherwise. Owning a home is not only rewarding, it can be a true wealth builder as well.

The only question is whether or not you can attain your piece of the American dream. A question can only be answered if you ask it.

Get Pre-Approved and Buy a Home like a Cash Buyer

Related Posts

- 70These figures are illustrations only. Prices are based on U.S median average sales prices, rates are reflective of a 30 year fixed rate loan for 1981 and early in 2013. Principal and Interest payments are based on an 80% loan to value, taxes are based on a factor of 1.5%…

- 69The “renter’s nation” is increasingly being used by pundits to describe the US housing market. If you go to the source, middle-class Americans, you’ll get a different story. Despite what you may hear, the myth that we are quickly becoming a “renter’s nation” is just that – a myth. According to…

- 69What difference does a mere $1,000 make on the housing market? Apparently, it makes all the difference in the world. Housing affordability has been a commonly touched subject for us recently. I have written about it several times because it concerns me. I find it to be a disconcerting topic. The housing affordability…

- 64It’s not a great time to be a renter. In fact, it might be the worst time in 36 years. The median rent nationwide now takes up 30.2 percent of the median American income, the highest cost burden recorded since 1979. In the late 1980s and throughout the 1990s, the…

- 45Republican lawmakers unveiled the tax reform bill this morning and it doesn't augur well for housing. (** After the bill was passed, I wrote an updated version of this post. Please refer to that by clicking here - https://www.mortgageblog.com/5-ways-the-tax-cuts-and-jobs-act-will-impact-housing-and-mortgages/) The National Association of Realtors came out swinging against the bill, suggesting…