Is the American Dream of Home-ownership, Just a Dream?

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

The “renter’s nation” is increasingly being used by pundits to describe the US housing market.

If you go to the source, middle-class Americans, you’ll get a different story. Despite what you may hear, the myth that we are quickly becoming a “renter’s nation” is just that – a myth.

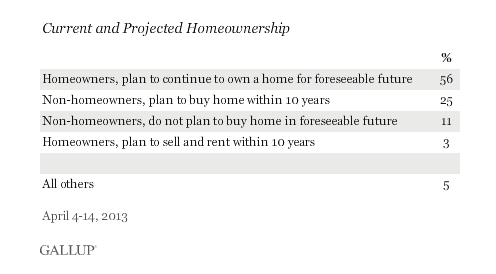

According to Gallup, the numbers clearly suggest quite the opposite. When polled, only slightly over 1/10th of the population completely spurn the idea of home-ownership altogether.

Household income is the primary predicator when it comes to opinions on the importance of owning a home. It seems obvious – most people who can afford to own a home already own one or plan to buy very soon.

Three-quarters of those making at least $75,000 a year own their home and plan on continuing to own, while another 15% say they will buy a home within the next 10 years.

Still, it is apparent that the hope of being able to buy a house is relatively strong even in the minds of those with below-average incomes, given that between 35% and 40% of Americans making less than $50,000 a year say that while they currently don’t own a home, they plan on buying one in the future.

There is plenty of positivity surrounding home-ownership. The American dream is still the American dream – to those who can afford it. Might pundit cynicism on housing be misplaced?

Is the American dream of home-ownership just that – a dream – or is it based in reality? Can we really afford the dream?

In most U.S. markets, the majority of homes for sale are within reach of the middle class and buying is cheaper than renting in all of the 100 largest metros.

However, in many markets, especially along the coasts, homeownership is still out of reach for the middle class. Even having a college degree is no guarantee that homeownership is within reach in the priciest markets.

And yet, Gallup data on homeownership provide strong support for the idea that the American Dream of owning a home continues to thrive.

These results show that the primary reasons why Americans don’t own are financial rather than cynical. There lies the center of the Housing Market – Home Affordability.

To truly analyze a subjective subject like housing affordability is complex. However, failing to analyze home affordability can have drastic results. Results that we are still trying remedy from the great Housing Crash and Great Recession of 2007.

Making housing more affordable is a difficult task. If you lower home values you do so at the expense of current home-owners. When they sell their home they net less than expected, nothing at all or they actually have to liquidate assets in order to complete the sale. Assets they would have quite possibly used toward the down payment on a new home.

With fewer assets to apply toward their next down payment, sellers turned buyers require higher loan to-values and become a riskier bet for mortgage lenders. Few loans are made and few homes are sold as a result.

What solutions do we have? Catching up with the inventory glut by building new construction (at the right pace) is step one. Incentivizing housing construction would be a good idea. Assuming, of course, we learned our over-indulgence lesson from the past decade.

However, in some markets like most of the California Coast and New York City, adding inventory will only dent housing affordability issues. How can we solve their dilemma? Is it even solvable?

Finding a savvy mortgage consultant who can deliver creative mortgage options is a must in all markets, but especially in the pricier ones like California. The right loan officer can also introduce you to a sharp real estate agent with a keen eye for value and potential.

So let’s have the affordability discussion and figure out YOUR options. Let’s do it now too. With home prices on the rise and higher interest rates looming there is no time like the present.

Click HERE to connect for a free pre-approval and rate quote.

Related Posts

- 69What do you do when the free market prices the average - sometimes even the exceptional - American family out of owning a home? The answer used to be simple, people would just rent. In many markets - most major metro area - rents are increasing at rates equal to,…

- 67What difference does a mere $1,000 make on the housing market? Apparently, it makes all the difference in the world. Housing affordability has been a commonly touched subject for us recently. I have written about it several times because it concerns me. I find it to be a disconcerting topic. The housing affordability…

- 62It’s not a great time to be a renter. In fact, it might be the worst time in 36 years. The median rent nationwide now takes up 30.2 percent of the median American income, the highest cost burden recorded since 1979. In the late 1980s and throughout the 1990s, the…

- 58These figures are illustrations only. Prices are based on U.S median average sales prices, rates are reflective of a 30 year fixed rate loan for 1981 and early in 2013. Principal and Interest payments are based on an 80% loan to value, taxes are based on a factor of 1.5%…

- 56Republican lawmakers unveiled the tax reform bill this morning and it doesn't augur well for housing. (** After the bill was passed, I wrote an updated version of this post. Please refer to that by clicking here - https://www.mortgageblog.com/5-ways-the-tax-cuts-and-jobs-act-will-impact-housing-and-mortgages/) The National Association of Realtors came out swinging against the bill, suggesting…