What to Do in a Changing Real Estate and Mortgage Market

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

As if the shortage of homes for sale wasn’t severe enough, now rising interest rates are making the spring buying season extra challenging across the nation. The latest analysis and forecasting of market information by organizations such as National Association of Realtors (NAR), the St. Louis Federal Reserve, and Realtor.com highlights the shortage in inventory. Meanwhile, the California Association of Realtors (CAR) is reporting some good news in California.

Read on to get the latest data, but don’t take it all as a sign that you should abandon your plans to buy or sell a home. You just need to know what to do in a changing real estate and mortgage market to beat the odds.

Get a customized rate quote for your next Mortgage

The Data Picture

First, here’s what the latest data says:

According to realtor.com, nationally, the inventory of home listings declined at a slower pace in May. “This May, the market showed a slightly larger than usual seasonal increase in inventory, and grew 6 percent over April, more than the 4 percent average increase in previous Mays since 2012. Additionally, although inventory was down 6 percent over last May, this rate of decrease is slower than the 9 percent average decrease in the previous 12 months.”

NAR’s chief economist Lawrence Yun, reacting to data from April, “The root cause of the underperforming sales activity in much of the country so far this year continues to be the utter lack of available listings on the market to meet the strong demand for buying a home.”

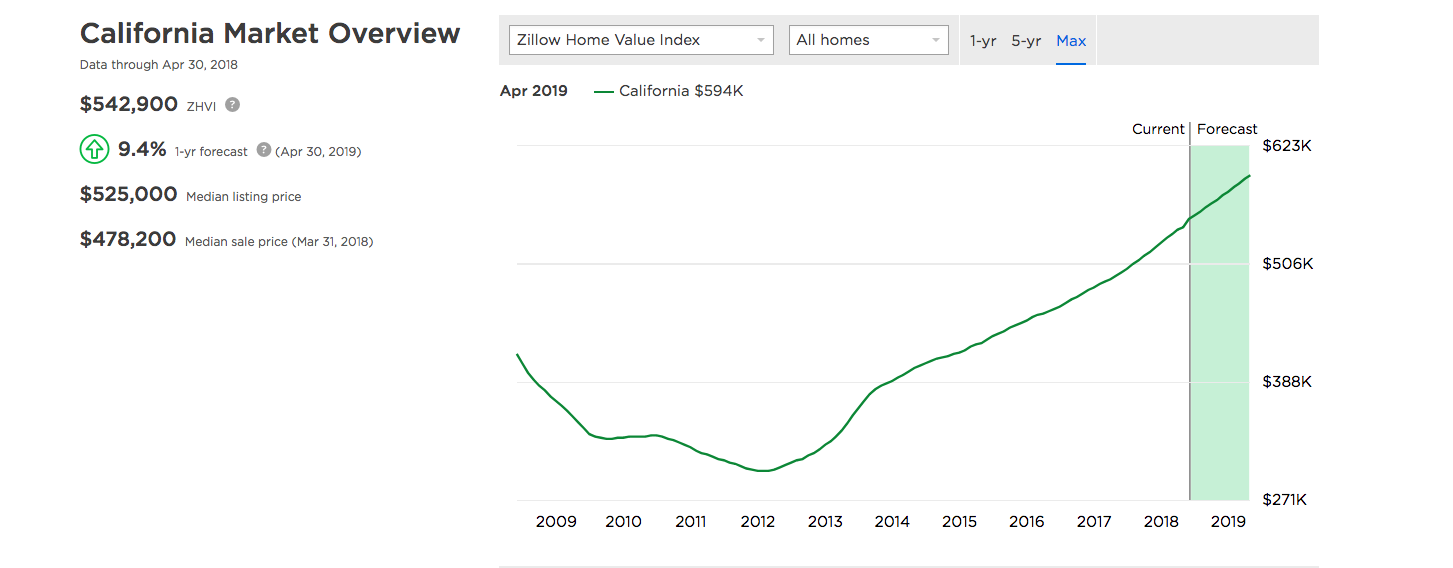

Statistics from Zillow focusing on the California market overview, projected into April 2019, predicts a 9.4% increase in median home prices as seen in the chart below.

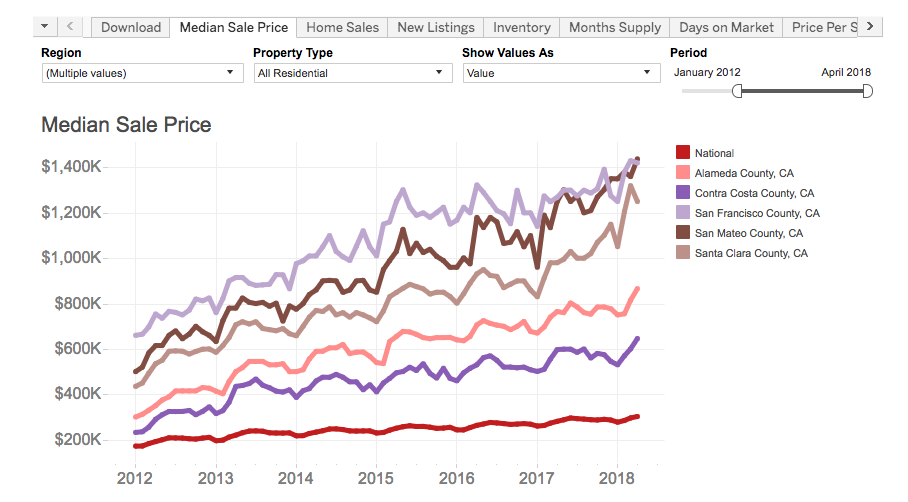

While the following chart from the St. Louis Federal Reserve compares the median sales price in the five Bay Area counties to the nation.

This data is also confirmed by Fannie Mae in their May 2018 Economic Developments.

California had some good news last month in C.A.R.’s April 2018 resale housing report, with President Steve White stating “After nearly three years of decline in active listings, we’re finally seeing an improvement in the availability of homes for sale, which is encouraging for prospective buyers as we enter the busy spring home-buying season.” This increase applied to homes above $300,000.

C.A.R. Senior Vice President and Chief Economist Leslie Appleton-Young commented on median sales prices in California now close to the pre-recession median value. “After increasing year-over-year by more than 8 percent for the past three months, the California median home price is close to striking distance of the pre-recession peak price of $594,530, which was recorded in May 2007.”

Also in C.A.R.’s report:

- “On a regionwide, non-seasonally adjusted basis, all major regions recorded both solid month-to-month and year-over-year sales gains. The San Francisco Bay Area led the way with a 6.0 percent monthly increase and 6.1 percent annual increase.”

- “The Bay Area continued to lead the state in sales, with Alameda recording a double-digit annual sales gain of 14.5 percent. Santa Clara, Contra Costa, and Sonoma also recorded healthy annual sales gains of 8.7 percent, 7.1 percent, and 6.8 percent, respectively.”

- Despite median home prices well exceeding $1 million in the Bay Area, sales remained robust in April as the region’s median price increased 14.1 percent from a revised $885,000 last April to $1,010,000 in April 2018. Prices in six of nine counties increased double-digits on a year-over-year basis.”

What You Can Do

With mortgage rates nearing their predicted level of 5% by the fourth quarter of 2018, now is the best time to buy a home. Even though they’re increasing now, interest rates won’t be this low again for years. Locking in the lowest interest rate you can, as soon as you can, is the most critical step you can take, but not the first step.

Also, be as ready as you can be before you become an active buyer. Now is the time to do all the things that you’ve heard and read about becoming mortgage ready. Check your credit and work on any issues you find. Conserve your cash for the down payment and closing costs by diverting excess funds from debt reduction into savings.

You’ll need to have the source of the money you estimate you’ll need to be identified and ready. This can include your savings, a gift from family, a pending bonus, or possibly a loan from your retirement account. Wherever your money is coming from, think it through and research any steps to gather the funds that aren’t currently in your accounts.

At the same time, interview lenders and choose one to work with so you can begin the credit approval process. The credit approval process is different than a full mortgage approval because it happens before you have a property. A buyer with a full credit approval, compared to a formal pre-approval, can potentially compete with cash buyers. Aside from an appraisal and possible review of a homeowners association, they’re ready to close their mortgage loan quickly.

Get Pre-approved for buying your first home or the next Home

Once you’re completely ready and credit approved, interview real estate agents that are active in the area you’ve targeted. Pick one to work with and begin the final steps of getting educated on what your credit approved loan amount and cash can purchase. Be sure to pay attention to the market value of the homes and not the list price.

Follow these steps, and you’ll be locking in contract on the home of your dreams and locking in an interest rate before you know it.