A Complete Guide to VA Streamline Refinance (IRRRL)

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

VA Streamline refinances are also called the Interest Rate Reduction Refinance Loan (VA IRRRL).

Are you eligible for a VA Streamline Refinance (IRRRL)?

If you currently have a VA loan and would like to (and why wouldn’t you?) lower your interest rate and/or monthly payments – you should consider a VA streamline refinance.

To be eligible for a VA IRRRL, you only need 3 things – You should currently have a VA loan, you currently live or have lived in this home, and you should be current on your mortgage with no more than one 30-day late in the last 12 months.

What are the Benefits of a VA IRRRL?

VA IRRRLs are probably the easiest mortgage out there, no wonder they are called “streamline refinance”.

- You do not need to provide any income documentation.

- There is no home appraisal required. So, it doesn’t matter what is the current value of your home.

- A bank/asset documentation is not required if your cash to close is $0.

- The new rate and the monthly payment will be lower than your previous payment. This doesn’t necessarily apply if you are moving from a Adjustable Rate Mortgage (ARM) to a Fixed Rate Mortgage.

What is the Funding Fee for a VA Streamline Refinance?

Unless you are exempt, the VA funding fee for all streamline refinances is 0.5% of the loan amount. The fee is added to the loan amount, so you do not need to bring this money as closing cost.

So if your base loan amount is $200,000, you can add 0.5% (=$1,000) to the loan amount, making it a total of $201,000.

What is the rate and closing cost for a VA IRRRL?

VA Streamline Refinances have one of the lowest rates out of all mortgage programs. At Arcus Lending, we offer extremely competitive rates to our veterans for refinancing their mortgages. Get a live rate quote

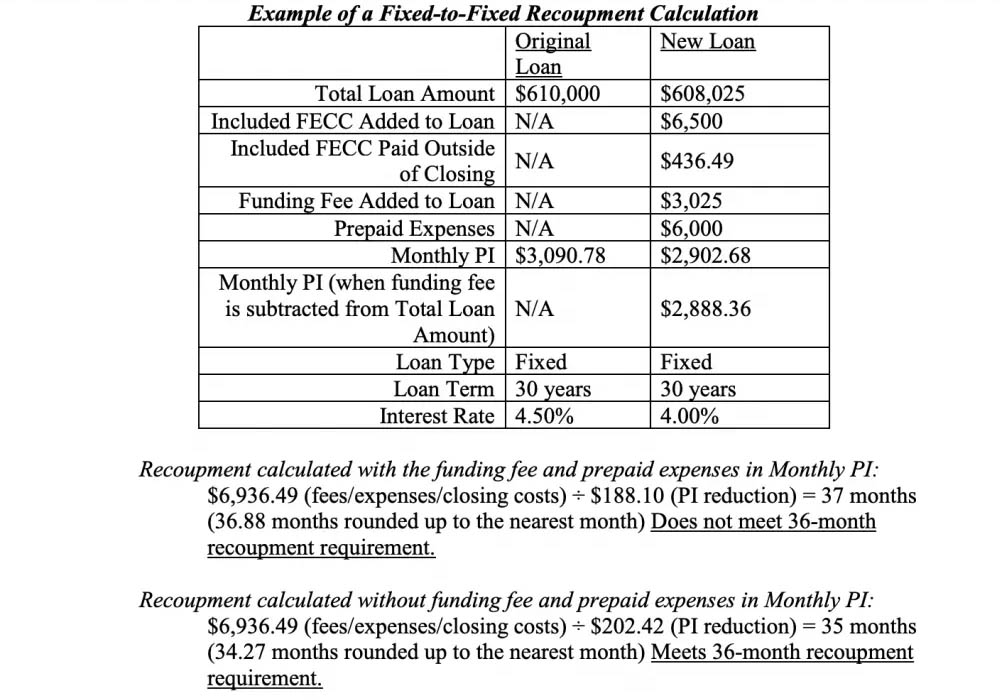

Any closing cost paid during the refinance has to be recouped in 36 months. Fees, expenses, and closing costs (FECC) to be recouped are lender fees including credit report, and discount points. Excluded in FECC are costs like VA funding fee, per diem interest, escrow, and pre-paid charges for home insurance, property tax, etc.

See the example below:

Can I get Cash-out with a VA Streamline Refinance?

Cashouts are not allowed with VA IRRRLs. However, you can get up to $6,000 as part of Energy Efficient Mortgage (EEM) which you can use to remodel your home with allowable energy-efficient upgrades.

Also, if you are adding the prepaid (impound) reserves for property taxes and insurance as part of the new loan, your current escrow balance will be refunded to you by the lender a few weeks after the new refinance closes.

InstaMortgage is an approved VA Lender with stellar reviews and very aggressive VA IRRRL interest rates. Get started with your VA Streamline Refinance application today.