The Complete Guide to Qualifying for the Home Possible Program

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

Saving to buy a home while you watch prices and interest rates increase feels like an impossible goal. You checked into FHA loans and learned it only requires 3 ½% of the purchase price as a down payment. But then you learned about the high, and permanent, mortgage insurance premiums. No thanks.

Well, don’t give up on your dream of homeownership! Consider these loans offered by Freddie Mac: the Home Possible loan requiring a minimum of 5% (of the purchase price) down payment and the Home Possible Advantage, allowing a minimum of 3% (of the purchase price) as the down payment.

The best news is that Freddie Mac is making it easier to qualify for both loans beginning October 29, 2018.

Embracing Mortgage Insurance

Yes, both loans require you to pay Mortgage Insurance premiums, but the cost is less than an FHA loan. The other difference from an FHA loan is you can drop the mortgage insurance once there is 20% equity in the property. Equity accumulated by a combination of loan repayment and property appreciation.

You’ll need to check with a lender for the exact cost of the monthly premium paid along with your mortgage payment. Or, consider Lender Paid Mortgage Insurance (LPMI), if available, to eliminate monthly premiums. (Doing this requires a slightly higher interest rate but better tax benefits.)

These loan programs represent a great opportunity in today’s real estate market – no matter where you live. So how do you know if you qualify? Use this complete guide then call your lender to get your individual questions answered!

Get Pre-Approved to buy your First Home

Save For a 3% Down Payment

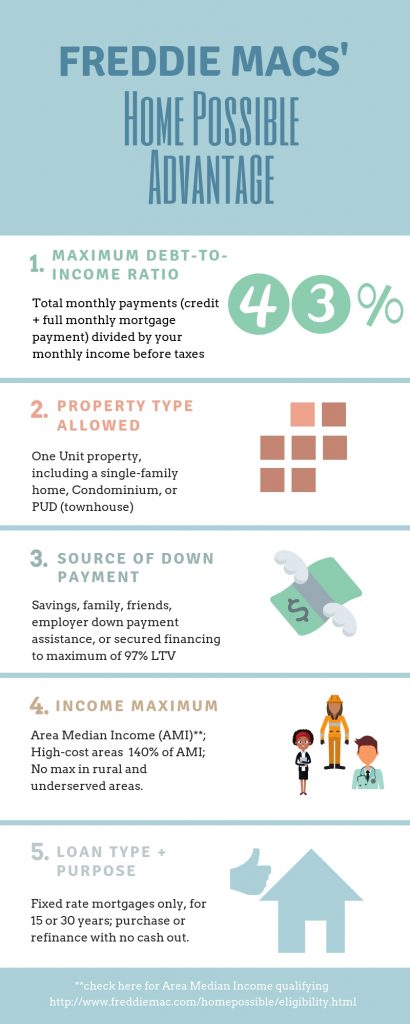

With a down payment of 3% of the purchase price, you may qualify for a Home Possible Advantage loan under these circumstances:

More details about qualifying for the Home Possible Advantage include: it must be your primary residence, no vacation or rental properties allowed. Typical minimum credit scores are 620, check with your lender to confirm. There are more qualifying criteria that both Freddie Mac loan programs have in common, but let’s talk about qualifying for the Home Possible loan first.

Save For a 5% Down Payment

If you’ve been able to save or accumulate 5% of the purchase price of a home, you are eligible for the Home Possible loan under these circumstances:

The main difference with Home Possible are:

- A 5% down payment is required.

- Can be used to purchase a one-four unit property.

- Allows a higher debt-to-income ratio of 45%.

You can also borrow a higher loan amount with 5% minimum down payment – up to the high-balance limit in your area – as long as you meet the other qualifying criteria detailed above.

The Home Possible program has another advantage – the ability to qualify without a credit score. You’re limited to a fixed rate, a conforming loan amount (high balance conforming not allowed) and a one unit single family home, condo or PUD. (No manufactured homes allowed.)

Note – you can only qualify without a credit score with zero collections (except medical), judgments, or tax liens reported within the previous 24 months. You’ll need to take the homeownership education program offered by Freddie Mac (at least one of all borrowers must complete), which available online. You’ll receive a certificate when you finish it and will need to give it to your lender before they prepare the loan documents.

Get Pre-Approved for the Home Possible Loan Program

New For Both Loan Programs

Freddie Mac’s changes to the Home Possible and Advantage programs become effective November 1, 2018. One change addresses qualifying with Student Loan debt. Updated guidelines allow lenders to use the monthly payment shown on your credit report to qualify you.

If the monthly payment for your student loan isn’t on your credit report, lenders will use 0.5% of the remaining balance of the student loan to calculate a payment for qualifying. They can do this even if your student loan is in deferred status, or in Forbearance. Previously, you had to gather documentation confirming the actual (non-reported) payment – or a much higher monthly payment calculation prevailed!

Another update is the ability to own other property and still qualify. There are no restrictions on owning other property with these guideline changes. In the past, the only way you qualified owning other property is if you either:

Inherited an interest in a property and were not the sole owner.

It’s property you own with another, and they retained the property in a divorce.

You were only a co-signor on a mortgage loan, and the other party made the payments for a minimum of 12 consecutive months.

Sharing Ownership

Freddie Mac now allows someone to be on the title of a home (partial ownership) even if they don’t live in the property with you. This is a significant change from previous guidelines. It’s not uncommon to have someone share the title with you on your home, even if they will never occupy the house with you. While it won’t contribute to helping you qualify for the loan if your situation dictates that you have to share the title – it’s no longer a roadblock.

If you’re someone who needs to have another person on the title that won’t be living in the property, you will need to:

- Make a minimum of 5% down payment

- Purchase a one-unit (single family, condo, or PUD)

- Qualify with a maximum debt-to-income ratio of 43%

There are no reserve requirements for either program unless you purchase a 2-4 unit property. In that case, two full months of the mortgage payment must be available in your assets after you close the loan. To clarify – in addition to the down payment, closing, and pre-paid costs, you need excess funds equal to two months of the mortgage payment in a checking/saving/investment account.

Having an in-depth conversation with a lender is the best way to discover if this is the right program for you.

Related Posts

- 93Haven't saved quite enough money for a down payment on a home? How about zero money of your own saved, but your family will gift you money towards a down payment? Or maybe there's no possibility of receiving a gift of money from anyone in your family - but you…

- 85Most lenders will require that you have homeowners insurance in place before the closing. This is also be called hazard insurance because it covers natural disasters like fire and storms, and theft. Why do you need insurance for a house? The lender won't fund the loan on a property that…

- 84What is home inspection? A home inspection- is a limited examination of a home's condition and is done when a home is put on the market for sale. State Laws do not require to have a home inspection or the number of inspectors you should bring. But even if the…

- 84Why you need Home Warranty? For many new owners, this is a great way to gain peace of mind about problems that they used to call the landlord to fix; ones that often aren't covered under their homeowner's insurance. But make sure you read your contract carefully to see what…

- 83Somethings in life take a little preparation. Like going on a first date, decorating for the holidays, and applying for a mortgage. Imagine the outcome if you did zero prep work for the first two occasions? So why do so many people miss the obvious fact that applying for a…