Getting a Mortgage has suddenly become Hard (and about to get even Harder)

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

Mortgage credit supply decreased 16 percent in March to the lowest level since June 2015, with declines in availability across all loan types. There was a reduction in the availability of loans with lower credit scores and higher LTV ratios, and the largest pullback came from the jumbo and non-QM space.

With the mortgage market shaken badly by the Coronavirus pandemic, both purchasing and refinance loans have become harder to get. JP Morgan believes that at 10% unemployment, we may be looking at 2 million new mortgage delinquencies. The number could go up to 5.5 million if the unemployment rate climbs to 15%.

Such high unemployment numbers can have only one kind of fallout- a huge pile of missed rental payments and mass forbearance. Foreclosures, at this stage, are not a big part of current economic debates but who knows how long they can be kept out of the mix.

Why are loans currently hard to get?

Unsurprisingly, the lenders are playing this one very cautiously.

Credit requirements have toughened a good deal. Lower loan-to-value ratio (LTV), lower debt-to-income ratio, and higher credit scores are becoming the order of the day.

The Subprime loans of a decade back that had come with a new name, the Nonprime loans, had lately created a much-debated but useful alternate market. These loans are also facing a lot of obstacles now. The Nonprime or the Non-QM mortgages (non-qualified) are harder to offload as they are not legally protected. That the lenders know such loans can’t be sold to Fannie Mae or Freddie Mac have made these loans less attractive for them. These loans have dissipated overnight with all non-QM lenders suspending loan closings or shutting shops altogether.

While conforming mortgages might still be procured without too much fuss, jumbo refinances are facing maximum resistance. For the record, the conforming loan limit is $510,400 for a majority of markets, with expensive counties ceiled at $765,600.

Traditionally speaking, counties with ‘Conforming’ limit $510,400 won’t be hit very hard even if the jumbo loans were to disappear for a while. The ‘jumbo’ pain will be badly felt by the high-cost counties (with a Conforming loan limit of $765,600) like the San Francisco Bay Area, Washington DC, Boston, or New York, to name a few. After all, there aren’t many investors willing to pick such risky tabs.

Liquidity has become the top concern. True, the Fed is working tirelessly towards purchasing a big pile of Conforming mortgage-backed bonds. This, however, does not soak the pressure of the overall lending space. Investors, playing safe at this hour, are retreating fast from the Non-QM and Jumbo space. They can’t be blamed. They don’t know if there is any money to be had in this market, even at a later stage. They are unsure how long the interruptions are expected to continue or what may be the implications for their business portfolio.

Government loans like FHA and VA, have seen their minimum credit score requirement increase from 500 to 640 or even 660 or 680 depending on the lender. Chase announced a minimum credit score requirement of 700 across all mortgage loan products, simultaneously requiring a 20% down payment, for nearly all borrowers.

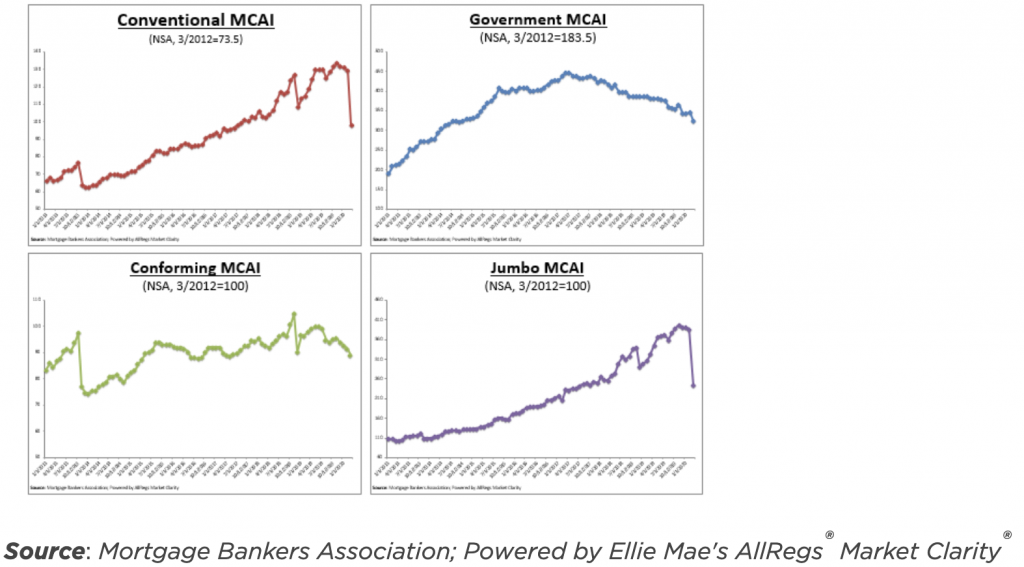

The Mortgage Credit Availability Index (MCAI) offers an interesting insight for the Jumbo loans. MCAI goes high in times of loose lending because the credit availability is higher. When lending norms tighten, the credit availability shrinks, thus bringing MCAI down with it. The Jumbo loans, which cannot be sold to Government-sponsored bodies like Fannie Mae or Freddie Mac, have seen their MCAI come down by 36.9% from Feb to March. To gain perspective, the Conforming MCAI (covered by ‘Fannie’ and “Freddie’) has come down by only 2.7% within this period.

Why could loans become even harder to get?

Delinquencies are not a big problem in times of rising home values. At such times, lenders are assured that the homeowners could always sell their homes to cover the mortgage delinquency. But with Covid-19 corroding the home values, and causing unemployment that may further corrode home prices, both the lenders and investors are jittery about the expected delinquency.

The 10%-15% unemployment picture that JP Morgan has painted (and mind you, some worst-case estimates are pointing at 20% unemployment) means that it may take months or even years for the market to return to normalcy. Note that it took 2 years for 2 million delinquencies to surface during the 2008 crisis. This is the time of Covid-19. We don’t talk years. We talk weeks. Yes, it is that bad.

As if these obstacles were not enough, the turn-time for loan closing has increased quite tellingly. There are lenders quoting 5 months turn around time to close on a refinance. Covid-19 has forced-shut Title companies. The appraisers and notaries are finding it equally difficult to operate. Borrowers themselves are uncomfortable letting a stranger into their homes. In the months leading to the pandemic, record-low interest rates had boosted refinance volumes. In a sad unfolding of events, even those applications largely await rejections now. Why? Because the borrowers may not qualify anymore if the home values go down or if they lose their jobs or even request a forbearance.

Will it get any better?

All the problems impacting the credit availability can take months even years to fix. Remember during the 2008 recession, it took almost 4 years for the real estate markets to stabilize. This time the projections are much severe.

One thing is certain – mortgage rates for any loan other than a high credit score, primary residence, or Conforming Loan Balance of $510,400 will not go down. Investment properties, cash-out loans, jumbo Loans, high balance loans, low credit score loans – they are all considered too risky to lend to because of a lack of demand for these loans in the secondary market.

If you have a locked interest rate, try to do everything at your end to close. Once you lose the lock, your opportunities would be bare. If you haven’t locked your rate yet, be in touch with your mortgage advisor to find an opportunity to lock. And when you find one, don’t wait too greedily for the rate to fall down further.

This is not the time to be greedy, this is the time to be prudent.