FHA Wont Allow Cancellation Of Mortgage Insurance Anymore; Increases Premium

Author bio section

I am the author of this blog and also a top-producing Loan Officer and CEO of InstaMortgage Inc, the fastest-growing mortgage company in America. All the advice is based on my experience of helping thousands of homebuyers and homeowners. We are a mortgage company and will help you with all your mortgage needs. Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies.

FHA recently announced changes to mortgage insurance premium for home loans insured by the agency. The new guidelines will make FHA loans more expensive. You will also need to pay mortgage insurance for the life of the loan in most cases.

Changes to FHA Annual Mortgage Insurance Premium

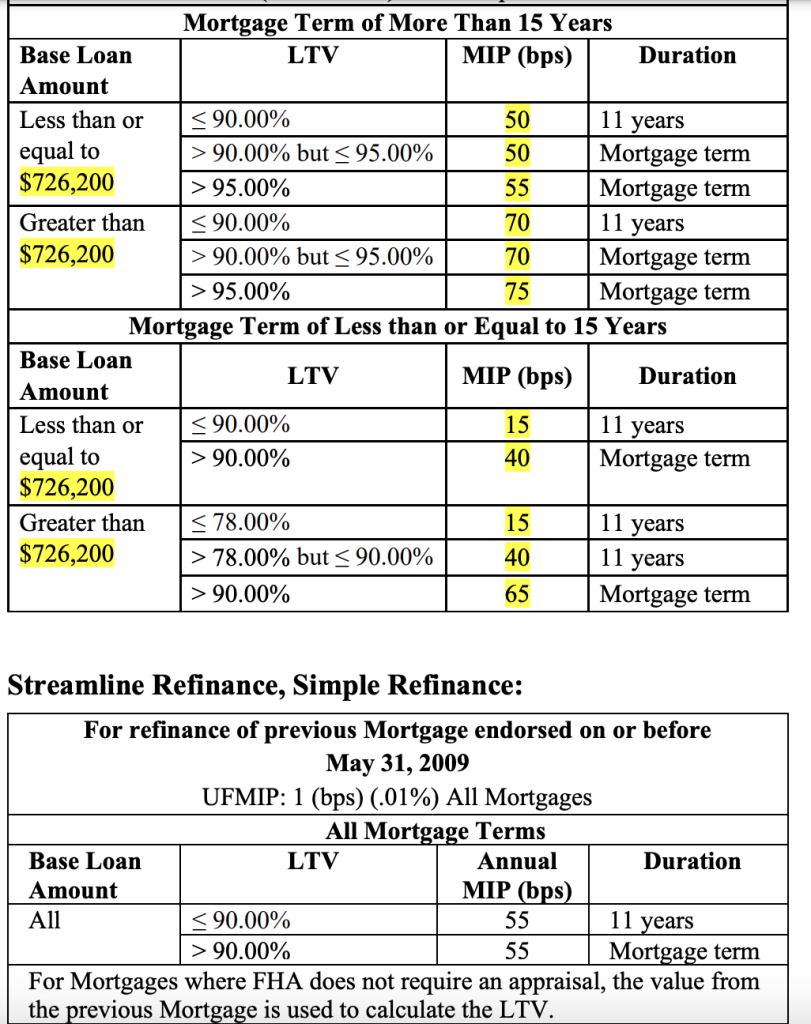

The below chart shows the changes coming to FHA mortgage insurance premium. This goes into effect for loan applications on or after March 1, 2023.

Can I cancel FHA Mortgage Insurance Premium?

- For all mortgages regardless of their amortization terms, any mortgage involving an original principal obligation (excluding financed Up-Front MIP (UFMIP)) less than or equal to 90 percent LTV, the annual MIP will have to be paid until the end of the mortgage term or for the first 11 years of the mortgage term, whichever occurs first.

- For any mortgage involving an original principal obligation (excluding financed UFMIP) with an LTV greater than 90 percent, FHA annual MIP will have to be paid until the end of the mortgage term or for the first 30 years of the term, whichever occurs first.

So if you are considering getting an FHA loan in California and rest of the country, it will make sense to do it before the new guidelines take effect. Get a Live FHA Rate Quote now!You may also like to read – Complete Guide to FHA Loan Requirements

So if you are considering getting an FHA loan in California and rest of the country, it will make sense to do it before the new guidelines take effect. Get a Live FHA Rate Quote now!You may also like to read – Complete Guide to FHA Loan Requirements